•Allianz Global Investors Fund (“AGIF”) as an umbrella fund under the UCITS regulations has within it different Sub-Funds investing in fixed income securities, equities, and derivative instruments, each with a different investment objective and/or risk profile.

•All Sub-Funds may invest in financial derivative instruments (“FDI”) which may expose to higher leverage, counterparty, liquidity, valuation, volatility, market and over the counter transaction risks. A Sub-Fund’s net derivative exposure may be up to 50% of its net asset value (“NAV”).

•Some Sub-Funds as part of their investments may invest in any one or a combination of the instruments such as fixed income securities, emerging market securities, and/or mortgage-backed securities, asset-backed securities, property-backed securities (especially REITs) and/or structured products and/or FDI, exposing to various potential risks (including leverage, counterparty, liquidity, valuation, volatility, market, fluctuations in the value of and the rental income received in respect of the underlying property, and over the counter transaction risks).

•Some Sub-Funds may invest in single countries or industry sectors (in particular small/mid cap companies) which may reduce risk diversification. Some Sub-Funds are exposed to significant risks which include investment/general market, country and region, emerging market (such as Mainland China), creditworthiness/credit rating/downgrading, default, asset allocation, interest rate, volatility and liquidity, counterparty, sovereign debt, valuation, credit rating agency, company-specific, currency (in particular RMB), RMB debt securities and Mainland China tax risks.

•Some Sub-Funds may invest in convertible bonds, high-yield, non-investment grade investments and unrated securities that may be subject to higher risks (including volatility, loss of principal and interest, creditworthiness and downgrading, default, interest rate, general market and liquidity risks) and therefore may adversely impact the net asset value of the Sub-Funds. Convertibles will be exposed prepayment risk, equity movement and greater volatility than straight bond investments.

•Some Sub-Funds may invest a significant portion of the assets in interest-bearing securities issued or guaranteed by a non-investment grade sovereign issuer (e.g. Philippines) and is subject to higher risks of liquidity, credit, concentration and default of the sovereign issuer as well as greater volatility and higher risk profile that may result in significant losses to the investors.

•Some Sub-Funds may invest in European countries. The economic and financial difficulties in Europe may get worse and adversely affect the Sub-Funds (such as increased volatility, liquidity and currency risks associated with investments in Europe).

•Some Sub-Funds may invest in the China A-Shares market, China B-Shares market and/or debt securities directly via the Stock Connect or the China Interbank Bond Market or Bond Connect or other foreign access regimes and/or other permitted means and/or indirectly through all eligible instruments and thus is subject to the associated risks (including quota limitations, change in rule and regulations, repatriation of the Sub-Fund’s monies, trade restrictions, clearing and settlement, China market volatility and uncertainty, China market volatility and uncertainty, potential clearing and/or settlement difficulties, change in economic, social and political policy in the PRC and Mainland China tax risks).

•Some Sub-Funds may adopt the following strategies, Socially Responsible Investment (Proprietary Scoring) Strategy, SDG-Aligned Strategy, Sustainability Key Performance Indicator Strategy (Relative), Green Bond Strategy, Multi Asset Sustainable Strategy, Sustainability Key Performance Indicator Strategy (Absolute Threshold), Environment, Social and Governance (“ESG”) Score Strategy, and Sustainability Key Performance Indicator Strategy (Absolute). The Sub-Funds may be exposed to sustainable investment risks relating to the strategies (such as foregoing opportunities to buy certain securities when it might otherwise be advantageous to do so, selling securities when it might be disadvantageous to do so, and/or relying on information and data from third party ESG research data providers and internal analyses which may be subjective, incomplete, inaccurate or unavailable and/or reducing risk diversifications compared to broadly based funds). Also, some Sub-Funds may be particularly focusing on the greenhouse gas emissions (“GHG”) efficiency of the investee companies rather than their financial performance. These may have an adverse impact on the performance of the Sub-Funds.

•Some Sub-Funds may invest in share class with fixed distribution percentage (Class AMf). Investors should note that fixed distribution percentage is not guaranteed. The share class is not an alternative to fixed interest paying investment. The percentage of distributions paid by these share classes is unrelated to expected or past income or returns of these share classes or the Sub-Funds. Distribution will continue even the Sub-Fund has negative returns and may adversely impact the net asset value of the Sub-Fund. Positive distribution yield does not imply positive return.

•Investment involves risks that could result in loss of part or entire amount of investors’ investment.

•In making investment decisions, investors should not rely solely on this [website/material].

Note:Dividend payments may, at the sole discretion of the Investment Manager, be made out of the Sub-Fund’s capital or effectively out of the Sub-Fund’s capital which represents a return or withdrawal of part of the amount investors originally invested and/or capital gains attributable to the original investment. This may result in an immediate decrease in the NAV per share and the capital of the Sub-Fund available for investment in the future and capital growth may be reduced,in particular for hedged share classes for which the distribution amount and NAV of any hedged share classes (HSC) may be adversely affected by differences in the interests rates of the reference currency of the HSC and the base currency of the respective Sub-Fund, particularly if such HSC are applying the IRD Neutral Policy. Dividend payments are applicable for Class A/AM/AMg/AMi/AMgi/AQ Dis (Annually/Monthly/Quarterly distribution) and for reference only but not guaranteed. Positive distribution yield does not imply positive return. For details, please refer to the Sub-Fund’s distribution policy disclosed in the offering documents.

Allianz Global Investors Asia Fund

•Allianz Global Investors Asia Fund (the “Trust”) is an umbrella unit trust constituted under the laws of Hong Kong pursuant to the Trust Deed. Allianz Thematic Income and Allianz Selection Income and Growth and Allianz Yield Plus Fund are the sub-funds of the Trust (each a “Sub-Fund”) investing in fixed income securities, equities and derivative instruments, each with a different investment objective and/or risk profile.

•Some Sub-Funds are exposed to significant risks which include investment/general market, company-specific, emerging market, creditworthiness/credit rating/downgrading, default, volatility and liquidity, valuation, sovereign debt, thematic concentration, thematic-based investment strategy, counterparty, interest rate changes, country and region, asset allocation risks and currency (such as exchange controls, in particular RMB), and the adverse impact on RMB share classes due to currency depreciation.

•A Sub-Fund may invest in asset-backed securities (“ABS”) and mortgage-backed securities (“MBS”) which may be highly illiquid and prone to substantial price volatility. These instruments may be subject to greater general market risk, concentration risk, credit and counterparty default risk, liquidity risk and interest rate risk compared to other debt securities.

•Some Sub-Funds may invest in high-yield (non-investment grade and unrated) investments and convertible bonds which may be subject to higher risks, such as volatility, creditworthiness, default, interest rate changes, general market and liquidity risks and therefore may adversely impact the net asset value of the Sub-Fund.

•All Sub-Funds may invest in financial derivative instruments (“FDI”) which may expose to higher leverage, counterparty, liquidity, valuation, volatility, market and over the counter transaction risks. The use of derivatives may result in losses to the Sub-Funds which are greater than the amount originally invested. A Sub-Fund’s net derivative exposure may be up to 50% of its net asset value (“NAV”).

•These investments may involve risks that could result in loss of part or entire amount of investors’ investment.

•In making investment decisions, investors should not rely solely on this website.

Note: Dividend payments may, at the sole discretion of the Investment Manager, be made out of the Sub-Fund’s income and/or capital which in the latter case represents a return or withdrawal of part of the amount investors originally invested and/or capital gains attributable to the original investment. This may result in an immediate decrease in the NAV per distribution unit and the capital of the Sub-Fund available for investment in the future and capital growth may be reduced, in particular for hedged share classes for which the distribution amount and NAV of any hedged share classes (HSC) may be adversely affected by differences in the interests rates of the reference currency of the HSC and the base currency of the Sub-Fund, particularly if such HSC are applying the IRD Neutral Policy. Dividend payments are applicable for Class A/AM/AMg/AMi/AMgi Dis (Annually/Monthly distribution) and for reference only but not guaranteed. Positive distribution yield does not imply positive return. For details, please refer to the Sub-Fund’s distribution policy disclosed in the offering documents.

Before you start investing, it is important to understand what you want to achieve. What is your investment objective? Are you looking to achieve mainly capital growth or income or capital preservation? What is your investment horizon? Are you looking to invest for one year, three years, five years or over a longer period? What is your risk tolerance? To what extent are you prepared to endure capital losses or erosion of real wealth through inflation?

It is also important to consider what, in general, are the key features of the various investment funds that are available to you. To what extent are they likely to provide capital growth or income? What are the main factors that drive their performance? How risky are they relative to other kinds of funds?

Step 3 - Choosing the Suitable Fund Mix

A successful investment strategy requires the right mix of funds. The selected fund options should match your main investment objectives and investor profile. Often the better outcome will involve several types of investment funds. By investing in a combination of different funds, you may reduce the overall level of risk through diversification: as one investment is performing badly, another investment may be performing well. The gains and losses are offset under normal circumstances, thereby reducing the risk.

Please click the image to view the enlarged version.

Generally, if an investor requires a higher potential return he must be prepared to expose himself to a higher level of risk.

Step 4 - Regular Review

Your investment needs may change over time and you should regularly review your financial situation and consider whether you need to change your strategy and fund investments. You might need to reassess your investment objective and your risk-taking level each time before choosing the investment strategy that meets your investment needs and then make changes to reflect your modified financial situation.

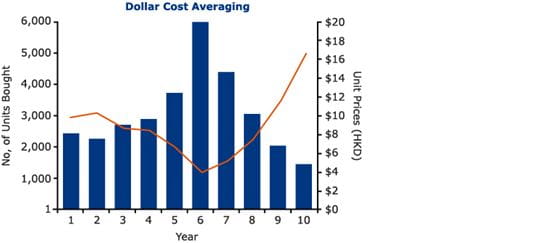

Dollar cost averaging is a technique designed to reduce market risk through regular investments at predetermined intervals and set amounts over time. By buying a fixed dollar amount of a particular investment on a regular schedule, regardless of the share price, investors can purchase more shares when prices are low and fewer shares when prices are high. Consequently, the impact of short-term market fluctuations on an investment can be mitigated and the costs of units purchased are averaged out.

This chart shows that if you invest HKD2,000 per month for 10 years, you buy more units when the price is low and fewer units when the price is high.

Hypothetical Example (Please click the image to view the enlarged version)

Dollar Cost Averaging

Lump Sum Investment

Rate of Return

(per annum)

8%

5%

Monthly Contribution

$2,000

-

Total Investment

$240,000

$240,000

Average Unit Cost

$7.83

($240,000/30,645units)

$10

Total Investment Value at Period End

30,645

24,000

Total Investment Value at Period End

$520,965

$408,000

According to the table, at the end of the period, the value of the total number of units bought is HKD520,965. This represents an annual rate of return of 8%, which amounts to returns almost 48% higher over the full 10 years when compared with a lump sum investment at the start of the period.

The above information used is for illustrative purposes only and are not indicative of any fund performance and the actual returns likely to be achieved by the investor.

Answer: A mutual fund pools money of many individual investors and a professional fund manager invests this pool of money in a wide range of investment instruments. Investors hold shares or "units" in the fund. The number of units an investor holds is based on the amount of money he or she invests. Fund unit is priced according to the value of the fund's investment at the close of the previous day.

Q2. What are the common investment instruments mutual funds invest in?

Answer: The most common investment instruments a mutual fund can invest in are - stocks, bonds and cash (e.g. bank deposits) all over the world. Some funds may also invest in derivative markets, such as futures and options markets.

Q3. How does investing in mutual funds benefit me?

Answer: It makes investing easy for you - once you decide which funds to invest in, you leave the day-to-day investment decisions to the professional managers. They not only take care of the complex and demanding tasks of market and investment instrument research but also the time-consuming administration work, like stock settlements. You can achieve asset diversification and benefit from high growth potential, as professional fund managers work for you to identify the best investment opportunities worldwide. A unit trust or fund generally invests in 50 to 100 different securities, often covering several different asset classes and/or individual national markets at once. This diversifies your investment a lot more efficiently than you can on your own.

Q4. Does investing in mutual funds mean that I give up control of my money?

Answer: No. You always have control of your investment. Firstly, it is your decision to invest in a specific fund and you make that decision based on your investment objectives. Secondly, you can always sell your units or switch to other funds on any dealing day.

Q5. Are there any mechanisms for mutual funds to control risks?

Answer: Basically, managing risk can be achieved in two ways – asset allocation and diversification. Different asset classes do not perform in the same way under different economic circumstances and mutual funds allow you to invest in different asset classes at once. For instance, high quality bonds might do well when stock markets are falling. Investing across shares, bonds and cash reduces portfolio risks and affords high potential return and relative stability. Other than diversifying across asset classes, a mutual fund also achieves diversification by investing in many different securities (usually 50 to 100) and different geographic markets. In this case, poor performance in one securities and one market does not do as much damage to the fund as it would if the entire portfolio is comprised of only a few securities from the same market.

Q6. What criteria should I consider when choosing a fund management company?

Answer: We believe a good fund management company should have the following qualities: market recognition, extensive global investment resources, proven performance track record, and strong customer focus with products and services tailored to clients' needs.

Q7. When is a good time to invest?

Answer: We believe the best way to invest is to start early and to take a long term and disciplined bottom-up investment approach with the focuses on earning growth and corporate fundamentals. In this sense, any time is a good time to start investing. The earlier you start, the earlier you benefit from the power of compounding effect. Remember, short-term volatilities in the market are hard if not impossible to predict.

Mutual funds, or unit trusts, are a pool of money from a number of investors. You are essentially able to buy a small stake in the mutual fund's underlying assets. By investing as a group with other investors, you may access a larger and more diversified pool of assets than you would as an individual.

Because the various expenses of investing (such as brokerage commissions, custodian's fees etc.) are spread over a larger pool of assets and effectively shared with all the other investors, mutual funds may provide you with a cost effective investment solution.

Another key benefit of mutual funds is that it is professionally managed. You have access to the same expertise as a large institutional investor. Your minimum investable money need only be a few thousand dollars, or even less.

Equity Funds

These focus mainly or exclusively on stock market investments, looking to achieve capital appreciation over the long term. Most equity funds seek to achieve defined capital growth objective in particular ways. Some focus on one particular stock market – such as Hong Kong. Others will invest in stock markets throughout a particular region of the world – such as the Asia Pacific – or worldwide.

Sometimes equity funds will be defined by the sort of companies that they invest in, rather than the part of the world that they are focusing on. Growth stocks, for instance, are investments in companies whose businesses and earnings are likely to expand at a relatively rapid rate. Value stocks, by contrast, are investments in companies that may pay attractive potential dividends and in turn appear to be cheap in terms of the valuations.

Bond Funds

Bond funds tend to focus mainly on fixed income investments, looking for long term capital appreciation and income. Many bond funds can and do provide some capital growth, and they are normally less risky than equity funds.

Bond funds are usually defined by the part of the world in which they invest, or the type of bonds in which they invest in. For instance, they may focus on government bonds. Alternatively, they may invest in corporate bonds, which are issued by large companies.

Most bonds are assessed for riskiness by major ratings agencies such as Standard & Poor’s or Moody's. Some bonds are seen by the agencies as being sufficiently risky that they are "below investment grade". Such bonds usually include high yield bonds and emerging markets debt.

Multi-asset Funds

Multi-asset funds combine a stock component, a bond component and, sometimes, a money market component, in a single portfolio. They look for a mixture of potential income and modest capital appreciation.

Cash or Liquidity Funds

Cash or liquidity funds are the least volatile of mutual funds. They invest in bank deposits and, sometimes, short-term bonds of very high quality. They usually carry no risk of capital losses, but offer no prospect of capital gain. Returns to investors come entirely from interest income.

Cash or liquidity funds are often attractive to investors who are very risk averse. Whilst they can also be useful as a place to park spare cash for a short period, it is not same as placing monies on deposit with a bank or deposit-taking company.

Diversification

Investing in funds provide you with the ability to build an enormous variety of portfolios. It is possible to spread your investments across stocks, bonds or cash or liquidity – or across a number of countries/locations, industries and sectors.

This diversification may reduce risk level, reduce volatility and increase the likelihood that your investments may produce a steady potential return over time.

By using mutual funds, you can build an investment portfolio that matches your investment objectives, risk tolerance and personal financial situation.

Fund Structure

Please click the image to view the enlarged version.

You are leaving this website and being re-directed to the below website. This does not imply any approval or endorsement of the information by Allianz Global Investors Asia Pacific Limited contained in the redirected website nor does Allianz Global Investors Asia Pacific Limited accept any responsibility or liability in connection with this hyperlink and the information contained herein. Please keep in mind that the redirected website may contain funds and strategies not authorized for offering to the public in your jurisdiction. Besides, please also take note on the redirected website’s terms and conditions, privacy and security policies, or other legal information. By clicking “Continue”, you confirm you acknowledge the details mentioned above and would like to continue accessing the redirected website. Please click “Stay here” if you have any concerns.

Welcome to Allianz Global Investors

Select your language

中文(繁體)

English

Select Role

Individual Investor

Intermediaries

Other Investors

Pension Investors

Allianz Global Investors Fund (“AGIF”)

•Allianz Global Investors Fund (“AGIF”) as an umbrella fund under the UCITS regulations has within it different Sub-Funds investing in fixed income securities, equities, and derivative instruments, each with a different investment objective and/or risk profile.

•All Sub-Funds may invest in financial derivative instruments (“FDI”) which may expose to higher leverage, counterparty, liquidity, valuation, volatility, market and over the counter transaction risks. A Sub-Fund’s net derivative exposure may be up to 50% of its net asset value (“NAV”).

•Some Sub-Funds as part of their investments may invest in any one or a combination of the instruments such as fixed income securities, emerging market securities, and/or mortgage-backed securities, asset-backed securities, property-backed securities (especially REITs) and/or structured products and/or FDI, exposing to various potential risks (including leverage, counterparty, liquidity, valuation, volatility, market, fluctuations in the value of and the rental income received in respect of the underlying property, and over the counter transaction risks).

•Some Sub-Funds may invest in single countries or industry sectors (in particular small/mid cap companies) which may reduce risk diversification. Some Sub-Funds are exposed to significant risks which include investment/general market, country and region, emerging market (such as Mainland China), creditworthiness/credit rating/downgrading, default, asset allocation, interest rate, volatility and liquidity, counterparty, sovereign debt, valuation, credit rating agency, company-specific, currency (in particular RMB), RMB debt securities and Mainland China tax risks.

•Some Sub-Funds may invest in convertible bonds, high-yield, non-investment grade investments and unrated securities that may be subject to higher risks (including volatility, loss of principal and interest, creditworthiness and downgrading, default, interest rate, general market and liquidity risks) and therefore may adversely impact the net asset value of the Sub-Funds. Convertibles will be exposed prepayment risk, equity movement and greater volatility than straight bond investments.

•Some Sub-Funds may invest a significant portion of the assets in interest-bearing securities issued or guaranteed by a non-investment grade sovereign issuer (e.g. Philippines) and is subject to higher risks of liquidity, credit, concentration and default of the sovereign issuer as well as greater volatility and higher risk profile that may result in significant losses to the investors.

•Some Sub-Funds may invest in European countries. The economic and financial difficulties in Europe may get worse and adversely affect the Sub-Funds (such as increased volatility, liquidity and currency risks associated with investments in Europe).

•Some Sub-Funds may invest in the China A-Shares market, China B-Shares market and/or debt securities directly via the Stock Connect or the China Interbank Bond Market or Bond Connect or other foreign access regimes and/or other permitted means and/or indirectly through all eligible instruments and thus is subject to the associated risks (including quota limitations, change in rule and regulations, repatriation of the Sub-Fund’s monies, trade restrictions, clearing and settlement, China market volatility and uncertainty, China market volatility and uncertainty, potential clearing and/or settlement difficulties, change in economic, social and political policy in the PRC and Mainland China tax risks).

•Some Sub-Funds may adopt the following strategies, Socially Responsible Investment (Proprietary Scoring) Strategy, SDG-Aligned Strategy, Sustainability Key Performance Indicator Strategy (Relative), Green Bond Strategy, Multi Asset Sustainable Strategy, Sustainability Key Performance Indicator Strategy (Absolute Threshold), Environment, Social and Governance (“ESG”) Score Strategy, and Sustainability Key Performance Indicator Strategy (Absolute). The Sub-Funds may be exposed to sustainable investment risks relating to the strategies (such as foregoing opportunities to buy certain securities when it might otherwise be advantageous to do so, selling securities when it might be disadvantageous to do so, and/or relying on information and data from third party ESG research data providers and internal analyses which may be subjective, incomplete, inaccurate or unavailable and/or reducing risk diversifications compared to broadly based funds). Also, some Sub-Funds may be particularly focusing on the greenhouse gas emissions (“GHG”) efficiency of the investee companies rather than their financial performance. These may have an adverse impact on the performance of the Sub-Funds.

•Some Sub-Funds may invest in share class with fixed distribution percentage (Class AMf). Investors should note that fixed distribution percentage is not guaranteed. The share class is not an alternative to fixed interest paying investment. The percentage of distributions paid by these share classes is unrelated to expected or past income or returns of these share classes or the Sub-Funds. Distribution will continue even the Sub-Fund has negative returns and may adversely impact the net asset value of the Sub-Fund. Positive distribution yield does not imply positive return.

•Investment involves risks that could result in loss of part or entire amount of investors’ investment.

•In making investment decisions, investors should not rely solely on this [website/material].

Note:Dividend payments may, at the sole discretion of the Investment Manager, be made out of the Sub-Fund’s capital or effectively out of the Sub-Fund’s capital which represents a return or withdrawal of part of the amount investors originally invested and/or capital gains attributable to the original investment. This may result in an immediate decrease in the NAV per share and the capital of the Sub-Fund available for investment in the future and capital growth may be reduced,in particular for hedged share classes for which the distribution amount and NAV of any hedged share classes (HSC) may be adversely affected by differences in the interests rates of the reference currency of the HSC and the base currency of the respective Sub-Fund, particularly if such HSC are applying the IRD Neutral Policy. Dividend payments are applicable for Class A/AM/AMg/AMi/AMgi/AQ Dis (Annually/Monthly/Quarterly distribution) and for reference only but not guaranteed. Positive distribution yield does not imply positive return. For details, please refer to the Sub-Fund’s distribution policy disclosed in the offering documents.

Allianz Global Investors Asia Fund

•Allianz Global Investors Asia Fund (the “Trust”) is an umbrella unit trust constituted under the laws of Hong Kong pursuant to the Trust Deed. Allianz Thematic Income and Allianz Selection Income and Growth and Allianz Yield Plus Fund are the sub-funds of the Trust (each a “Sub-Fund”) investing in fixed income securities, equities and derivative instruments, each with a different investment objective and/or risk profile.

•Some Sub-Funds are exposed to significant risks which include investment/general market, company-specific, emerging market, creditworthiness/credit rating/downgrading, default, volatility and liquidity, valuation, sovereign debt, thematic concentration, thematic-based investment strategy, counterparty, interest rate changes, country and region, asset allocation risks and currency (such as exchange controls, in particular RMB), and the adverse impact on RMB share classes due to currency depreciation.

•A Sub-Fund may invest in asset-backed securities (“ABS”) and mortgage-backed securities (“MBS”) which may be highly illiquid and prone to substantial price volatility. These instruments may be subject to greater general market risk, concentration risk, credit and counterparty default risk, liquidity risk and interest rate risk compared to other debt securities.

•Some Sub-Funds may invest in high-yield (non-investment grade and unrated) investments and convertible bonds which may be subject to higher risks, such as volatility, creditworthiness, default, interest rate changes, general market and liquidity risks and therefore may adversely impact the net asset value of the Sub-Fund.

•All Sub-Funds may invest in financial derivative instruments (“FDI”) which may expose to higher leverage, counterparty, liquidity, valuation, volatility, market and over the counter transaction risks. The use of derivatives may result in losses to the Sub-Funds which are greater than the amount originally invested. A Sub-Fund’s net derivative exposure may be up to 50% of its net asset value (“NAV”).

•These investments may involve risks that could result in loss of part or entire amount of investors’ investment.

•In making investment decisions, investors should not rely solely on this website.

Note: Dividend payments may, at the sole discretion of the Investment Manager, be made out of the Sub-Fund’s income and/or capital which in the latter case represents a return or withdrawal of part of the amount investors originally invested and/or capital gains attributable to the original investment. This may result in an immediate decrease in the NAV per distribution unit and the capital of the Sub-Fund available for investment in the future and capital growth may be reduced, in particular for hedged share classes for which the distribution amount and NAV of any hedged share classes (HSC) may be adversely affected by differences in the interests rates of the reference currency of the HSC and the base currency of the Sub-Fund, particularly if such HSC are applying the IRD Neutral Policy. Dividend payments are applicable for Class A/AM/AMg/AMi/AMgi Dis (Annually/Monthly distribution) and for reference only but not guaranteed. Positive distribution yield does not imply positive return. For details, please refer to the Sub-Fund’s distribution policy disclosed in the offering documents.

Please indicate you have read and understood the Important Notice.

External Twitter Content

This Twitter component is loaded through Twitter . Google is collecting information about your interaction with this Twitter by using cookies and may use this for targeting their offers. Please accept cookies in order to show the video.

Remember Me Cookie Dependent Disclosure

This Twitter component is loaded through Twitter . Google is collecting information about your interaction with this Twitter by using cookies and may use this for targeting their offers. Please accept cookies in order to show the video.